ESG ETFs - What’s in them and do they really represent ESG principles?

ETFs (Exchange Traded Funds) have been around for quite a while, however they have grown in popularity over the past several years. ETFs are low cost funds that track indices and require little management, meaning they are cheaper for the investor than owning a mutual fund or building their own personal portfolio of companies. ETFs are also easy to trade: You can buy and sell them just as you would a stock, so long as there are enough buyers and sellers out there to trade with you. The transactional ease and low cost has meant that the demand for ETFs has grown significantly, and has opened doors for organizations to put together funds that represent many different investment theses. Every bank, financial firm, and even individuals with a fund idea want to claim their piece of this market.

The growing interest in reflecting political, social, and environmental views through one’s investment portfolio has also been around for a long time. Think about the many divestment campaigns that have occurred throughout recent history. Even Yahoo Finance now includes a “Sustainability” tab on each company page, which present ratings from Sustainalytics that attempt to quantify ESG (environmental, social, and governance) strategies within firms (see an example here).

If an investor decides he or she should have a diversified portfolio reflecting the total market, an S&P 500 index ETF might be the best option. However, if that individual does not want to support, for example, oil and gas, tobacco, and firearms companies by holding their stocks, he or she needs to seek out some alternative to the major S&P 500 ETF. This is where ESG ETFs come in.

What are ESG ETFs?

What is considered an ESG ETF turns out to be a pretty broad category of investment products. Because environmental, social and governance factors can encompass many different aspects of how companies do business, the category can include anything from ETFs that include groups of companies screened for their gender diversity practices (SHE), to ETFs that include companies with practices that align with a religion’s principles (BIBL). There is even a fund with the ticker MAGA, which, as you may imagine, screens for companies that have made contributions to the GOP.

For this analysis, I used etf.com’s “Socially Responsible” category, which includes 81 different ETFs, 34 of which include only US-based companies. Due to data issues with a few of the ETFs and in order to streamline the analysis around a single country’s stock market, 27 ETFs were included in the full analysis, a list of ETFs that includes a total of 2,050 different companies.1 Below is a list of the ESG funds included in this analysis, along with their primary screening driver.

| Fund | Fund Name | Main Screening Driver |

|---|---|---|

| BIBL | Inspire 100 ETF | Biblical values; large-cap |

| CHGX | Change Finance U.S. Large Cap Fossil Fuel Free ETF | ESG conscious; large-cap |

| DSI | iShares MSCI KLD 400 Social ETF | Socially conscious |

| ESG | FlexShares STOXX U.S. ESG Impact Index Fund | ESG conscious |

| ESGL | Oppenheimer ESG Revenue ETF | ESG conscious; aims to beat S&P500 |

| ESGS | Columbia Sustainable U.S. Equity Income ETF | ESG conscious; aims for dividend characteristics |

| ESGU | iShares ESG MSCI U.S.A. ETF | ESG conscious; market-like exposure |

| ESGV | Vanguard ESG U.S. Stock ETF | ESG conscious; market-like exposure |

| ESML | iShares ESG MSCI U.S.A. Small-Cap ETF | ESG conscious; small-cap |

| ETHO | Etho Climate Leadership U.S. ETF | ESG conscious; companies with least carbon impact in industry |

| HONR | InsightShares Patriotic Employers ETF | Veteran-friendly; large-and mid-cap |

| ICAN | SerenityShares Impact ETF | ESG conscious |

| ISMD | Inspire Small/Mid Cap Impact ETF | Biblical values; small-and mid-cap |

| JPBI | James Purpose Based Investment ETF | Biblical values |

| JUST | Goldman Sachs JUST U.S. Large Cap Equity ETF | Public perception; large-cap |

| MAGA | Point Bridge GOP Stock Tracker ETF | GOP campaign contributions |

| MXDU | Nationwide Maximum Diversification U.S. Core Equity ETF | Socially conscious; targets minimum covariance between constituents |

| NULG | NuShares ESG Large-Cap Growth ETF | ESG conscious; large-cap growth |

| NULV | NuShares ESG Large-Cap Value ETF | ESG conscious; large-cap value |

| NUMG | NuShares ESG Mid-Cap Growth ETF | ESG conscious; mid-cap growth |

| NUMV | NuShares ESG Mid-Cap Value ETF | ESG conscious; mid-cap value |

| NUSC | NuShares ESG Small-Cap ETF | ESG conscious; small-cap |

| PRID | InsightShares LGBT Employment Equality ETF | LGBT equality |

| SHE | SPDR SSGA Gender Diversity Index ETF | Women on board of directors/execs; large cap |

| SPY | SPDR S&P 500 ETF Trust | S&P500 |

| SPYX | SPDR S&P 500 Fossil Fuel Reserves Free ETF | S&P500, excluding companies with fossil fuel reserves |

| SUSA | iShares MSCI U.S.A. ESG Select ETF | ESG conscious |

| VETS | Pacer Military Times Best Employers ETF | Veteran-friendly |

In my previous post, I dug a little deeper into what exactly ESG ETFs are, including an anecdote of some interaction I had with Vanguard regarding their ETF.

How are ESG ETFs designed?

All of the funds analyzed here track different underlying indices, indices which were designed by evaluating and screening for different characteristics. MSCI offers a lot of detail on this topic on their ESG ratings website, and they also provide the indices for many of these funds. Most of these screening algorithms are proprietary and not at all transparent, but luckily for us, they must report their portfolios and weightings. The weightings strategies within each index also follow different guidelines that have their own pros and cons.

There are two main types of ESG fund design. The first recognizes environmental, social, and governance risks and builds a portfolio of companies intended to minimized the fund’s exposure to those risks. The second is structured more like a typical ETF, but excludes companies in certain industries.

There is certainly an opportunity here to dig deeper into what is published about the methodologies and screening practices, but what I wanted to get at in this post was how the resulting indices available on the market today translate for the customer in terms of portfolio composition.

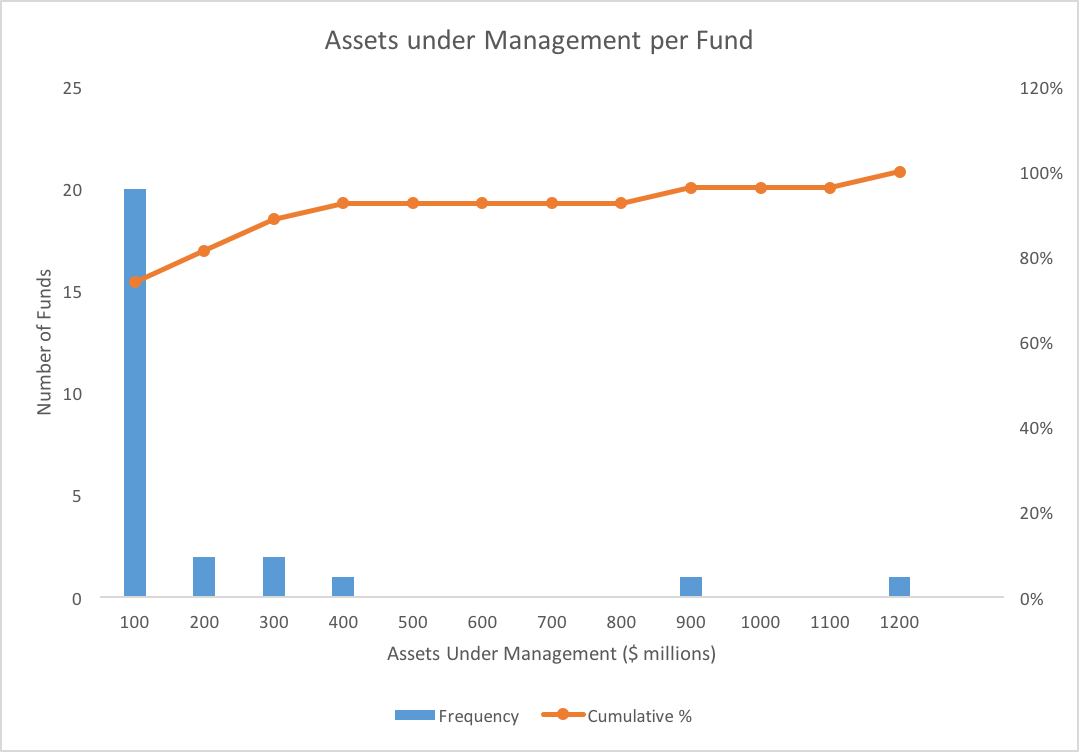

How big are these ETFs?

The ETFs analyzed here vary in size from only a few million to over $1 billion assets under management. Many of these funds are run by big banks (Blackrock, UBS, State Street, Goldman Sachs) with the corresponding big client lists with big cash flows, while others are run by much smaller outfits. I was surprised at just how small some of these ETFs were.

What industries, sectors, and specific companies are in these ETFs?

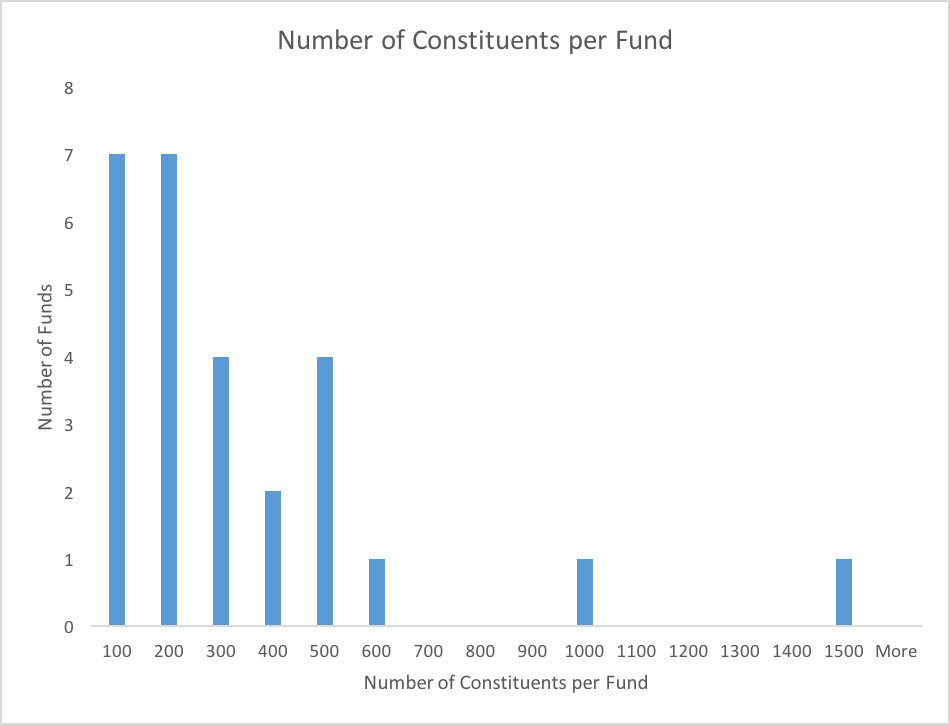

This was the question I really wanted to answer when I started looking at this data, which was triggered by Vanguard issuing their own ESG ETF, ESGV, which I discuss in my other post on this topic. Looking at a long list of funds is difficult as an individual, and since so many of these funds have hundreds of constituent assets, it takes a good bit of work to pit them all against each other and understand their similarities and differences.

I wanted to answer a couple of major questions with this data:

- Do many of these funds include a lot of the same companies, and do those companies already show up in my other holdings? I’m thinking here mostly of the FAMGA stocks (Facebook, Apple, Microsoft, Google, and Amazon), which, if you hold large-cap or large index-following funds like an S&P 500 tracking ETF, a big part of your portfolio may already be in these stocks. If I was going to buy into a new ETF, I wanted to make sure it was diversifying my savings a bit and not just buying MORE Apple, et al. stock.

- What industries are heavily weighted in these ETFs? Do those holdings follow the marketing for the ETF? For example, if the fund is supposed to exclude fossil fuels, does it?

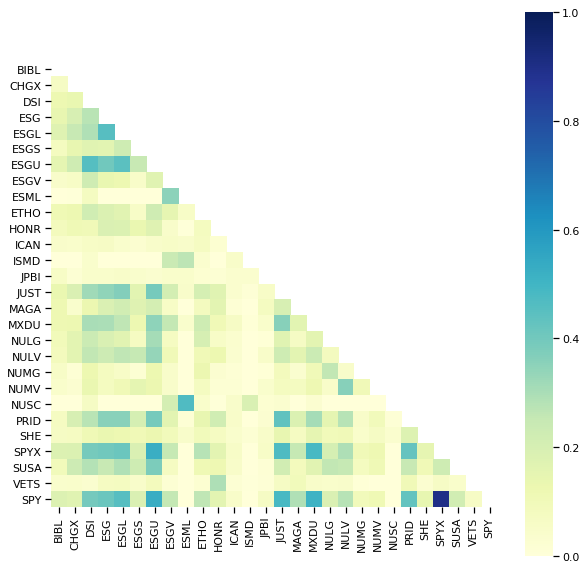

Evaluating fund similarity

To answer my first question, I used Jaccard similarity to compare each fund to all the other funds and understand how closely they match each other in terms of holdings. If a fund holds many of the same companies as another fund, it will show up darker on the plot. The result is striking.

As you can see from the matrix, the bluer a square is, the more similar it is to the corresponding fund. SPY is included as a baseline of sorts in the bottom row of this graphic: This ETF tracks the S&P 500 index. We can see in looking across this row that a few funds are more similar to SPY than others. ESGU, JUST, and MXDU are all very similar to SPY, and also to each other. Not surprisingly, SPYX and SPY are the funds with the most overlap.

As one might expect, some of the least similar funds are those that include only certain slices of the market, like companies that are small or mid-cap (NUMG, NUMV, NUSC). The single fund that is the least similar to all of the other funds turns out to be ISMD, which “tracks an equal-weighted index of 500 small-and mid-cap US stocks that are screened for alignment with biblical values and positive impact on the world according to various ESG criteria.”

Beyond observing how similar the funds were to one another, I also wanted to understand what was heavily weighted in these funds. Below is a list of the top 10 holdings of all the funds, sorted by average weight.

| Holding | Number of Funds with Holding | Average Holding Weight | Holding Weight in SPY |

|---|---|---|---|

| MICROSOFT CORP | 11 | 1.8% | 3.5% |

| APPLE INC | 13 | 1.5% | 3.3% |

| AMAZON.COM INC | 10 | 1.0% | 2.9% |

| VERIZON COMMUNICATIONS INC | 14 | 0.8% | 1.0% |

| COCA-COLA CO | 12 | 0.7% | 0.8% |

| MERCK & CO | 14 | 0.7% | 0.9% |

| PROCTER & GAMBLE CO | 14 | 0.7% | 1.1% |

| FACEBOOK INC | 11 | 0.7% | 1.8% |

| HOME DEPOT INC | 12 | 0.7% | 0.9% |

| JOHNSON & JOHNSON | 7 | 0.7% | 1.6% |

As we can see here, all of the FAMGA stocks except for Google show up high on this list, representing a large proportion of the total average holdings of these funds. The small-and mid-cap funds as well as the funds geared towards biblical values, which hold 0% of most of these companies, skew the average values lower when compared to SPY.

Evaluating portfolio composition

After understanding the similarity of some of these funds, I next wanted to learn more about what the screening claims translated to in terms of companies included in the portfolios. Several of the funds claim to exclude similar industries, with the most common being tobacco, oil and gas, and firearms. The most commonly screened industry of the funds analyzed was fossil fuels. Some funds are more specific (CHGX specifies that it excludes utilities that burn fossil fuels), and some are more vague (ESGV says that it excludes stocks in the fossil fuel industry). Since my initial review of ESGV from my last post led me down this path, I was interested in whether the fossil fuel claims of these portfolios did translate to excluding companies in the fossil fuel industry.

While many of these funds screen for ESG ratings, only a handful specifically call out excluding companies dealing in fossil fuels. The following list outlines these funds and their specific fossil fuel screening targets. All information has been gathered from the funds’ linked websites.

CHGX: Change Finance U.S. Large Cap Fossil Fuel Free ETF

- CHGX uses more than 50 different ESG criteria to exclude from its holdings:

- Companies operating in the oil, gas, coal, or tobacco industries

- Companies with a history of controversial business practice relating to human rights, labor rights (including, but not limited to, forced labor, child labor, and discrimination), environment, or business malpractice (including, but not limited to, corruption and taxes)

- Companies that produce nuclear power, GMOs, military weapons, or pesticides

- Utilities that burn fossil fuels

- Companies that produce or process fossil fuels

- Companies that fail to meet minimum standards related to other social and environmental impacts including, but not limited to, pollution, land use and biodiversity, renewable and alternative fuels, human trafficking, health impacts of products, and management of hazardous substances

ESGV: Vanguard ESG U.S. Stock ETF

- Seeks to track the performance of the FTSE US All Cap Choice Index.

- Market cap weighted index composed of large-, mid-, and small-capitalization stocks.

- Screened for certain environmental, social, and corporate governance (ESG) criteria.

- Specifically excludes stocks of companies in the following industries: adult entertainment, alcohol and tobacco, weapons, fossil fuels, gambling, and nuclear power.

- Excludes stocks of companies that do not meet standards of U.N. global compact principles and companies that do not meet diversity criteria.

ETHO: Etho Climate Leadership U.S. ETF

- Selects equities based primarily on an assessment of an equity’s carbon footprint.

- Seeks to provide investment results that, before fees and expenses, correspond generally to the price and yield performance of the Etho Climate Leadership Index U.S. (ECLI), a broadly diversified index of companies that have, on average, smaller carbon footprint in their industries.

ICAN: SerenityShares Impact ETF

- Beginning with a list of all 6500+ companies listed on the NYSE and NASDAQ, screens are applied to:

- Eliminate companies involved with tobacco; oil, gas, and coal exploration; and weapons, and

- Select companies that meet our market cap, price, and liquidity screens.

- We review all remaining companies to identify firms whose activities have a direct, beneficial impact that addresses the societal, social, or environmental challenges that govern the underlying index.

SPYX: SPDR S&P 500 Fossil Fuel Reserves Free ETF

- Serves as a potential replacement for current S&P 500 exposure for investors interested in eliminating fossil fuel reserves from their portfolio.

As it turns out, the composition of most of these funds seems to be aligned with my interpretation of their screening practices. Using a data set that included all of the funds listed above, their holdings, weightings, and industries, I filtered these funds for only the companies that fell into the following SIC industry categories: Oil & Gas Extraction, Petroleum & Coal Products, Coal Mining, and Pipelines. CHGX, ETHO, and ICAN all do not show up in the result because they do not hold companies in these categories. ESGV and SPYX do.

| Portfolio Weights | ESGV | SPYX |

|---|---|---|

| BAKER HUGHES A GE CO | 0.064% | 0.058% |

| C&J ENERGY SERVICES INC | 0.003% | |

| CORE LABORATORIES NV | 0.012% | |

| ENSCO PLC | 0.008% | |

| HALLIBURTON CO | 0.120% | |

| HELIX ENERGY SOLUTIONS GROUP | 0.003% | |

| HELMERICH & PAYNE | 0.050% | 0.026% |

| JAGGED PEAK ENERGY INC | 0.001% | |

| NABORS INDUSTRIES LTD | 0.004% | |

| NOBLE CORP PLC | 0.002% | |

| PATTERSON-UTI ENERGY INC | 0.009% | |

| PROPETRO HOLDING CORP | 0.007% | |

| ROWAN COMPANIES PLC | 0.005% | |

| RPC INC | 0.001% | |

| SCHLUMBERGER LTD | 0.279% | 0.255% |

| TECHNIPFMC PLC | 0.044% | |

| TRANSOCEAN LTD | 0.012% | |

| WEATHERFORD INTL PLC | 0.001% | |

| CARLISLE COS INC | 0.030% | |

| DELEK US HOLDINGS INC | 0.011% | |

| HOLLYFRONTIER CORP | 0.046% | |

| MARATHON PETROLEUM CORP | 0.195% | 0.201% |

| PHILLIPS 66 | 0.176% | 0.183% |

| QUAKER CHEMICAL CORP | 0.008% | |

| VALERO ENERGY CORP | 0.156% | 0.155% |

| VALVOLINE INC | 0.025% |

Because SPYX has been specific in what it excludes (companies with fossil reserves), it is not surprising that it does still include oilfield services and refining companies. What is more surprising is that of all of these funds that screen for fossil fuels, ESGV is the only one that seems to either not do it very well, or the index designers have chosen to be vague in order to still include many fossil fuel-related firms. While one could make some arguments about where you could draw the line, it seems that the line should be a bit further removed than this.

As far as tobacco product and firearms are concerned, one of the funds that claimed to exclude these industries (ESGV) did still include Axon Enterprise, maker of Taser, which is arguably a safer alternative to a firearm. While the following funds did not call-out tobacco and firearms as industries they were excluding, they might still be worth noting. ESML and NUSC also hold Axon Enterprise, and ESGL and SPYX hold tobacco firms Altria Group and Philip Morris. ESG holds only Altria Group.

How to use this data to inform a decision

There are many more ways we can look at all this data and compare one fund to another. From the few observations I’ve made with the data, how do I make a decision on where to invest?

One of the most important things to call out is that “impact investing” for the average individual looks very different than it does for someone of very high wealth or someone who could consider themselves an “accredited investor.” For most individuals, ETFs and public company portfolios put together by private companies like Swell Investing are the most accessible options. Either way, the investor is still only getting a piece of what’s available in the public markets. The average investor cannot easily put money into a company like Patagonia or a similar B Corp-type firm that is doing impactful work outside of their core business. Private companies have the benefit of being able to make decisions that might not necessarily be the best for the shareholders of the company, but may be the best for a broader spectrum of stakeholders. The general public can do little to support them financially besides being a customer and vocal advocate.

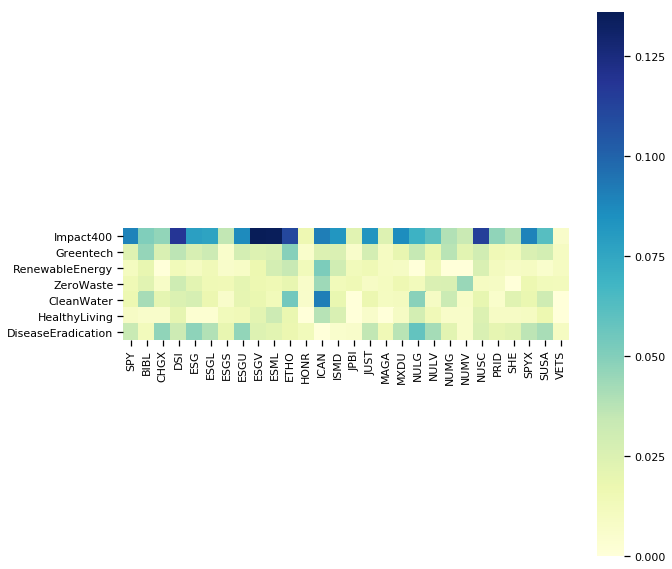

While we cannot easily invest in private firms that are using their businesses as a “force for good,” we do have a few other options outside of ETFs. One of those options is Swell Investing, which puts together portfolios that are targeted towards things like clean water, healthy living, and green tech. They have made an effort to diversify their portfolios and maximize returns while also maintaining focus on the goal of that fund. So what do those portfolios look like?

We can see from this plot that there is little overlap between the Swell funds and any of the ESG ETFs. Note the scale when considering the overlap that does appear with the Impact 400 Swell fund. This lack of significant overlap is to be expected: Many of the ETFs encompass a large number of companies, and those companies cover a broad range of industries, while Swell’s funds are by definition relatively focused on single industries.

Another option comes from a firm called Ellevest, which targets its investment products towards women. They offer full services to their clients similar to what you’d get at another investment company, but they gear their principles towards counteracting some of the implicit biases that exist in the financial services market. They also offer funds that claim an impact bent, however I was unable to see what is included in them without opening an account.

Conclusion

In the end, if an ETF of any sort struggles to match the returns of the broader market, that ETF will run the risk of losing investors and collapsing. To try to mitigate that, it is likely that the fund managers have chosen indices that maintain positions in industries and include companies that many may feel should be excluded. It seems relatively straightforward that these firms are trying to capture sustainability-conscious consumers by offering “ESG” focused funds, which makes it all the more important for the individual investor to really look at the holdings before making a decision to invest in one. If an investor has strong enough convictions about their savings that they would like to divest from certain companies or industries, those convictions should also be strong enough to ensure they are actually getting all they think they are.

-

ETF data was compiled by ETF Global and collected via Wharton Research Data Services (WRDS). The fund characteristics as of December 31, 2018 was used. ↩